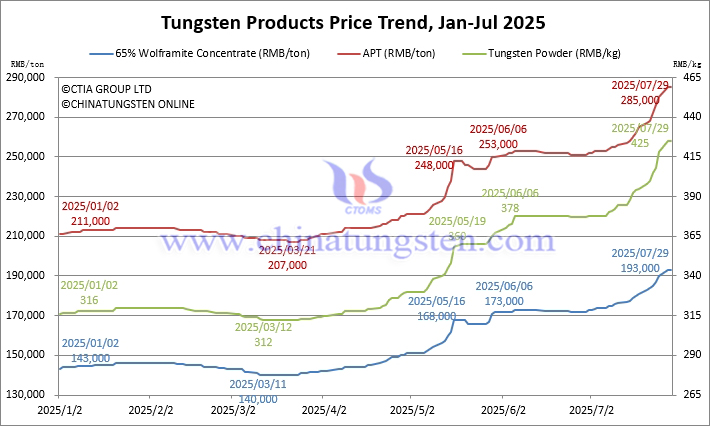

The current tungsten prices maintain a high-level trend, but potential market risks cannot be ignored. The pressure from supply-demand imbalances and structural contradictions is intertwined, urgently requiring coordinated efforts from policymakers and market entities to implement prudent measures and gradually promote industrial transformation and upgrading.

Key Factors Supporting Sustained High Tungsten Prices:

Declining Resource Endowment: Tungsten ore grade continues to decline, existing mines are depleting, and new mines are limited in supply, putting pressure on the supply side and, consequently, increasing mining costs.

Stricter Policy Controls: Export control measures have raised international concerns about China’s tungsten supply chain, driving global tungsten prices upward. The first batch of tungsten mining quotas this year was reduced, further tightening supply expectations. Additionally, China's “anti-involution” measures have standardized market order, indirectly supporting prices.

Rising Cost Pressures: Increased mining costs due to lower ore grades, combined with global inflation, labor, and logistics cost pressures, have driven up production and operational costs for tungsten product enterprises.

Elevated Strategic Importance: Amid rising global economic and geopolitical risks, resource security concerns have grown, leading to a revaluation and repricing of tungsten as a critical mineral.

Growing Emerging Demand: Expanding demand for tungsten and its products in sectors such as photovoltaics, new energy, semiconductors, and defense provides incremental market support.

Macroeconomic Support: Manufacturing and infrastructure investment are picking up, and major projects such as the hydropower project in the lower reaches of the Yarlung Zangbo River have enhanced tungsten demand expectations, providing both fundamental and sentiment-driven support.

Increased Capital Speculation: Tungsten’s strategic importance has attracted capital attention and intervention, with market sentiment and speculative behavior contributing to short-term price increases.

Accumulated Downside Risks from High Tungsten Prices:

Inefficient Cost Transmission: High upstream prices struggle to pass smoothly to downstream applications, squeezing profit margins in midstream smelting and deep processing, dampening procurement and production willingness. This increases operational pressures for mid- and downstream enterprises.

Overseas Capacity Recovery: High international tungsten prices are stimulating the restart or development of tungsten mining projects outside China. While new capacity is limited in the short term, long-term strategies in Europe and the U.S. to reduce reliance on Chinese resources could reshape the global supply landscape.

Suppressed Demand: Persistently high raw material prices are curbing actual downstream demand, potentially leading to delayed or canceled orders.

Threat of Substitute Materials: Rising tungsten raw material prices may spur the development and adoption of substitute materials. For instance, reduced substitution rates for tungsten wire in photovoltaics, and the potential for ceramics and silicon carbide to replace cemented carbide products in specific applications pose long-term threats to tungsten demand.

Economic Cycle Downturn: Global economies face challenges from inflation, monetary policy tightening, and geopolitical uncertainties. If major economies enter a recession, industrial demand, including for tungsten, will face widespread pressure, and tungsten prices will not be immune. Exchange rate fluctuations will also indirectly affect prices and enterprise operations.

Profit-Taking and Inventory Release: Current tungsten price increases are partly driven by trader hoarding and market speculation, with low physical market circulation. Once speculative inventories are released or market sentiment shifts, tungsten prices could see a rapid decline.