I. Tungsten Price Trend: All-Round Rise Breaks Through Historical Highs

This week, tungsten prices continued to rise strongly. After the long-term order prices of major tungsten companies were announced, the market's bullish sentiment increased. The supply of raw materials continued to be tight, pushing the prices of major products to continuously refresh historical highs. Affected by this, downstream deep-processing tungsten products passively followed the rise. However, end users have limited acceptance of high prices. Except for a small amount of rigid demand replenishment, the overall market order volume is scarce. Overall, this round of increases is mainly driven by supply contraction and market sentiment, rather than substantial improvements on the demand side.

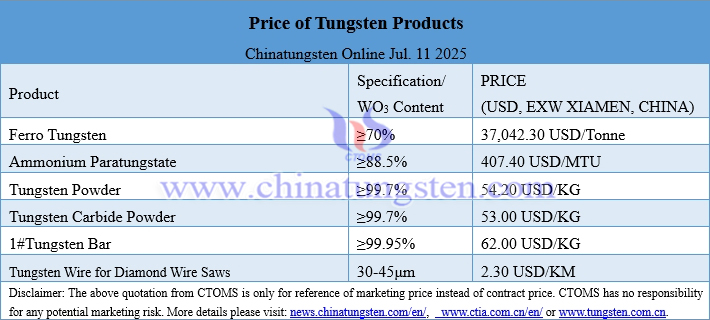

As of July 11, 2025,

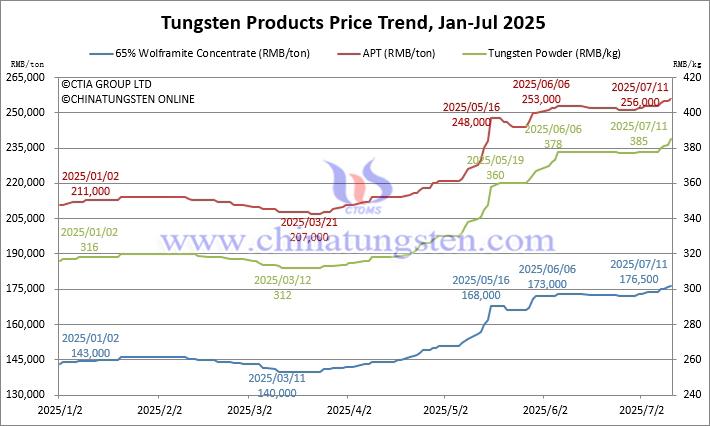

The price of 65% wolframite concentrate is RMB 176,500/ton, up 1.4% week-on-week and 23.4% from the beginning of the year.

The price of 65% scheelite concentrate is RMB 175,500/ton, up 1.5% week-on-week and 23.6% from the beginning of the year.

The price of ammonium paratungstate (APT) is RMB 256,000/ton, up 1.2% week-on-week and 21.3% from the beginning of the year.

The price of tungsten powder is RMB 385/kg, up 1.9% week-on-week and 21.8% from the beginning of the year.

The price of tungsten carbide powder is RMB 376/kg, up 1.4% week-on-week and 20.9% from the beginning of the year.

The price of 70 ferrotungsten is RMB 263,000/ton, up 1.9% week-on-week and 22.3% from the beginning of the year.

The price of scrap tungsten rods is RMB 264/kg, up 6.5% week-on-week and 20% from the beginning of the year.

The price of European APT is USD 440-485/ton, flat week-on-week and up 40.2% from the beginning of the year.

The price of European tungsten iron is USD 50.6-52/kg W, down 0.8% week-on-week and up 16.6% from the beginning of the year.

II. Tungsten Market Status: Supply and Demand Game Cautiously Shrinks Upward

Although the price of tungsten raw materials has risen significantly, the market transaction activity has not increased synchronously, reflecting the structural contradiction between supply and demand.

Supply Side: Resource Scarcity Supports Price Increase

Major mines are operating normally, and the expansion of profit margins has increased production enthusiasm. However, the quota restrictions on tungsten concentrate mining have laid the foundation for tight supply. Combined with geopolitical factors, the strategic value of tungsten as a safe-haven asset has been enhanced, and the market sentiment of the mine side is reluctant to sell and support the market. Resource scarcity is the core support for this round of price increases. We need to be vigilant about the potential competitive pressure brought by the expansion of overseas tungsten ore resources.

Demand Side: Rigid Demand and Cost Pressure Coexist

The actual demand performance is suppressed by the high raw material prices, especially the traditional manufacturing fields such as infrastructure, mechanical processing, and metal cutting are still facing the pressure of the sluggish economic environment. Small and medium-sized cemented carbide companies are generally facing the pressure of reducing production due to the difficulty in passing on costs, and the market share is accelerating to concentrate on the head companies. Despite this, the rigid demand in the military industry and strategic reserves provides certain support for the market. The demand for emerging industries has not yet been fully released, but the trend of the industry's transformation to a high value-added track is becoming more and more obvious.

III. Outlook for the Future Market: Short-Term High-Level Fluctuations and Long-Term Pattern Reshaping

In the short term, the tungsten market will maintain a high-level stalemate. Supporting factors include: mining quota restrictions, bullish sentiment support, and military orders are necessary. Downside risks come from: possible policy adjustments, weakened downstream demand, and increased profit-taking.

In the long run, resource scarcity and high raw material prices will accelerate the concentration of the tungsten industry, and market share will tilt toward leading companies and specialized and new companies. The proportion of tungsten consumption in new energy and military fields continues to expand, and the demand for high value-added products is growing. At the same time, tungsten resource efficient utilization technology (such as recycling and low-grade mine development) will usher in development opportunities and help the sustainable development of the industry.

In summary, the tungsten market continued to strengthen this week amid multiple contradictions: the conflict between supply rigidity and demand elasticity, the game between strategic value and economic cost, and the redistribution of interests between upstream and downstream of the industrial chain. These structural contradictions indicate that the tungsten industry is ushering in a new round of prosperity cycle, but it also contains the risk of technical correction after excessive price increases. While seizing strategic opportunities, market participants need to be wary of the operational challenges brought about by short-term fluctuations and build the ability to cross cycles through supply chain resilience and technological innovation.